The issue being examined is about the law applicable to sections 269ST and 271DA of the Income-tax Act, 1961. Whether the Penalty U/s 271DA For Violation Of S. 269ST Of The Income-tax Act, 1961 be levied on the Assessee or not?

Why was the bill introduced for Penalty U/s 271DA For Violation Of S. 269ST Of The Income-tax Act, 1961

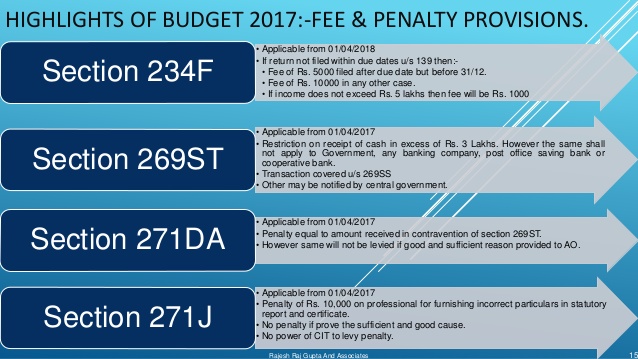

In order to curb black money and related unaccounted wealth and to achieve the vision of the Government to move towards a cashless economy, the Finance Act 2017 introduced new section 269ST w.e.f 01.04.17

What does the Law Stipulate regarding Cash Dealings u/s Sec 269ST?

Section 269SS and 269T of the I.T. Act, 1961 was introduced in the Act to prohibit the acceptance and repayment of loans/deposits/specified sums in cash in excess of Rs.19999/- with the intention to check the introduction of black money.

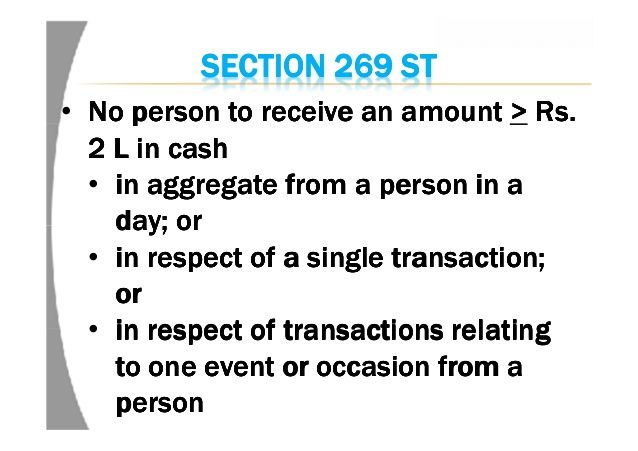

269ST w.e.f. 01.04.17 was amended to the effect that no person shall receive an amount of two lakh rupees or more

- In aggregate from a person in a day; or

- In respect of a single transaction; or

- In respect of transactions relating to one event or occasion from a person,

Otherwise than by an account payee cheque or an account payee bank draft or use of electronic clearing system through a bank account.

What does the Income Tax Act Stipulate in Sec 271DA?

If a person receives any sum in contravention of the provisions of section 269ST, he shall be liable to pay, by way of penalty, a sum equal to the amount of such receipt. Provided that no penalty shall be imposable if such person proves that there were good and sufficient reasons for the contravention.

Even if there is a technical violation of provisions of Section 269SS and Section 269T, as per settled judicial principals, no penalty u/s 271D or 271E is levied if,

- The transaction under question is genuine.

- The transaction is duly recorded in the books of the parties to the transaction.

- Identity and confirmation of the parties to the transaction is on record

- No black money/tax evasion/malaise intention is involved in the transaction

Generally, the Courts have been avoiding levy of penalty u/s 271D/271E for contravention of provisions of section 269SS/269T, by observing that the acceptance/ repayment of the loan in the cash being genuine and bona fide, there is a mere technical breach or venial violation.Hence penalty under section 271D/271E may not be imposed.

Like how it happened in the following case laws:

- Hindustan Steel Ltd V/s State of Orisa reported in 83 ITR 26.

- Bombay High Court in CIT vs. Triumph International Finance (345 ITR 270).

- Muslim Urban co-op Credit Society Ltd (2005) 96 ITD 83 (Pune),

- Karnataka Ginning And pressing factory v/s Jt CIT (77 ITD 478)

- Addl. CIT Vd Smt. Prahati Baruah (2003) 113 Taxman 74 (Gau)(Mag),

- Bhagwati Prasad Bajoriya 183 CTR 484, the Hon. Gauhati High Court

- Omec Engineers v/s CIT, reported in (2008) 217 CTR (Jharkhand) 144

Issues for consideration:

– Are favorable judgments’ rendered in context of section 269SS be still relevant for the purpose of application or otherwise of section 269ST r.w.s. 271DA?

– What could constitute “good and sufficient reason” so that penalty u/s 271DA is not levied for contravention of the provisions of section 269ST? And, is it same as “reasonable cause”?

Conclusion- Penalty u/s 271DA for violating section 269ST of Income Tax Act:

Therefore, if all the favorable ingredients as discussed above in the context of 269SS/269T are present in the transactions of the nature specified in section 269ST, judgments’ rendered in the context of section 269SS will surely be relevant for the purpose of application or otherwise of section 269ST r.w.s. 271DA.

However, these ingredients will be necessary but may not be sufficient to avoid the rigors of penalty u/s 271DA and court will look for further good and sufficient reasons to justify the contravention of S. 269ST. This is because proving the presence of good and sufficient reasons appears to be more onerous than proving the presence of reasonable cause.