Stock market highest returns and highest NAV are two different things

A 28 year old investor, Sankaran had invested in stocks, ULIPs and mutual funds. He was very happy when the stock market had touched 20000. But he incurred heavy losses when the stock market crashed down. This made him think that he should have en-cashed his investments when the market was at 20000. Lets find out how Stock market highest returns and highest NAV are two different things.

He, as expected, was blaming the stock market and wished that he could have been a little less greedy and should have sold his investments at 20k. Then he read an advertisement on a new ULIP scheme. It stated that it guarantees, the highest NAV for the initial seven years of the maturity period. The scheme claimed that despite a stock market crash, the company shall pay the highest NAV, guaranteed.

Now, what else did Sankaran want? He was very happy and went on to further investigate through the company’s brochure and also visited their website. All confirmed the news of guaranteed highest NAV irrespective of any stock market crash.

He definitely was very much attracted to the scheme, but before investment he still had his own doubts on how can a company promise highest NAV.

What does the term highest NAV actually mean?

He was just not satisfied with all the reasoning and answers he got from his relatives and friends. So he sought professional advice from a financial planner. So even if you are unclear on this topic, you are just at the right place.

The assumptions made by Sankaran and other people that highest NAV means the stock market’s highest return is wrong. Both the terms are entirely different and those who think it is the same. Please continue reading.

Think over the following points to find out how Stock market highest returns and highest NAV are two different things :

- Stock markets have crashed more than 50 percent of the time in the year 2000 and 2008. If a company would guarantee the highest returns despite of the crash, would not they go bankrupt?

- A company guaranteeing the highest rate in the first seven years of maturity will not face such a situation?

- One might claim to have understood the volatile nature of the stock market and might have achieved the extraordinary ability of predicting the stock market and will move out from the stock market well in advance. Well, in that case, why would he or she work in an insurance company?

- Will not such a person be on his own and make huge profits without revealing his secret to anybody?

- Why has no one provided such a guarantee earlier, ever?

- Why is this guarantee not provided on other schemes and only on ULIP?

Many, in fact, most of the insurance companies have provided such guaranteed schemes of highest NAV return. They all are not lying. They mean it when they say so. But the fine print is that they are promising the highest NAV of their schemes and not the highest stock market returns.

These are two different terms which are mistakenly assumed to be the same by the general public, or may be is presented in such a way that the general public gets mislead.

How do the schemes work?

These schemes are not required to invest your money in the stock market. They might invest very little or might not invest a single penny in the stock market. They invest most of the money or the entire amount in the debt market. And this investment will be made for the maximum tenure of the maturity period.

Now, here is how they assure highest NAV. The debt funds fetch you an interest of 8-10 percent per annum on your investment. So the promise of paying highest NAV is no rocket science. Any company will be in a position to pay the highest NAV of 10 percent in the case of a crash and downfall.

Old wine in a new bottle:

The ULIP schemes are the same as before. They were rejected by the public for higher entry charges which comes upto 20 to 40 percent of the first year premium. Which is very specific to invest in ULIPs only. The same public is now again getting attracted to the scheme as it is promising of highest NAV. And is ready to pay the same higher level of entry charges.

Basically, people forget the pitfalls of a product when the same product gets re-launched with a fancy idea.

A few simple investment rules:

- When you wish to make the most of the stock market return, you shall invest in the equity mutual funds and stay there for a long term, atleast for 5 years.

- Also, to get tax benefits along with good returns, invest in tax saving mutual funds. These funds have no entry charges like ULIPs.

- When you want to go for insurance coverage, you shall invest in term insurance policies. The term insurance policies and SIP in equity fund are a better option to the expensive ULIP schemes.

- When all you need is an assured return on your investment made, you can put your hard earned money in PPF, NSC and bank FDs.

Whatever scheme you invest in, always remember that the stock market return rates and the policy guarantee, are two different things and should not be mistaken to be the same. Hope, you all understood how Stock market highest returns and highest NAV are two different things.

Common mistakes people make after a criminal charge

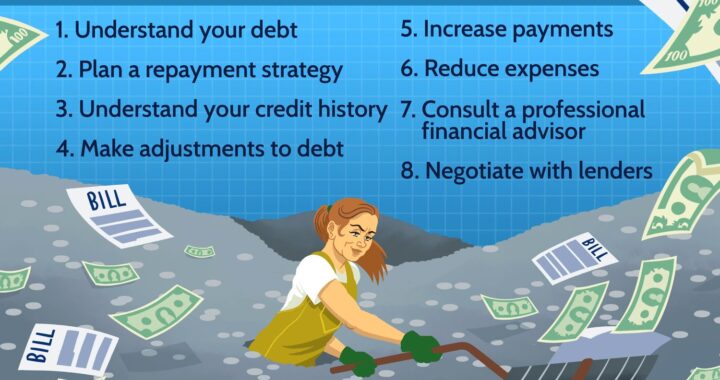

Common mistakes people make after a criminal charge  Take Control of Your Loans: Expert Strategies for Better Management

Take Control of Your Loans: Expert Strategies for Better Management  Dealing With a Workplace Accident

Dealing With a Workplace Accident  Qualities That Make For A Great Expert Witness

Qualities That Make For A Great Expert Witness  Marketing Business Ideas and Opportunities for Residual Income

Marketing Business Ideas and Opportunities for Residual Income  Supreme court Judgement: Tax Exemption Ambiguity-Benefit in favor of the Revenue Department

Supreme court Judgement: Tax Exemption Ambiguity-Benefit in favor of the Revenue Department  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?