Notice U/S 148 of the Income Tax Act, 1961 – assessment & reassessment

Notice u/s 148

The structure of the India Tax system is quite simple, detailed but differentiable in power among State, Central, and other local governments. There are some sections are mentioned in income tax Act, 1961, depending upon which type of tax you are paying. Organizations and individuals may get notices under any section if it seems necessary from income tax department. You can file itr online that is quite easiest way. Online itr file has benefits of no delays and less chances of losing posts.

Introduction to section 148 (Income-tax Act, 1961)

Section 147 of the Income tax Act, 1961 is provided for assessments/reassessments, if the officer finds that some income has escaped assessment for any assessment subject to provisions mentioned in Section 148 to Section 153. This is also known as Reopening and Reassessment. The assessing officer (A.O.) can assess this escaped income regarding which he is making a belief and also some other income (chargeable to tax) that is come to his notice during proceeding under section-148 or the depreciation allowance or re-computing the loss. For this purpose of making re-opening or Reassessment, a notice u/s.148 is necessary to be issued just after recording the reasons in writing for issuance. This notice is issued, directing the aassesee to file income tax return online.

Assessing officer should examine the information. Thus the information must be specific, clear and having nexus with the assessee. Most importantly, this information must be available at the time of reassessment or reopening.

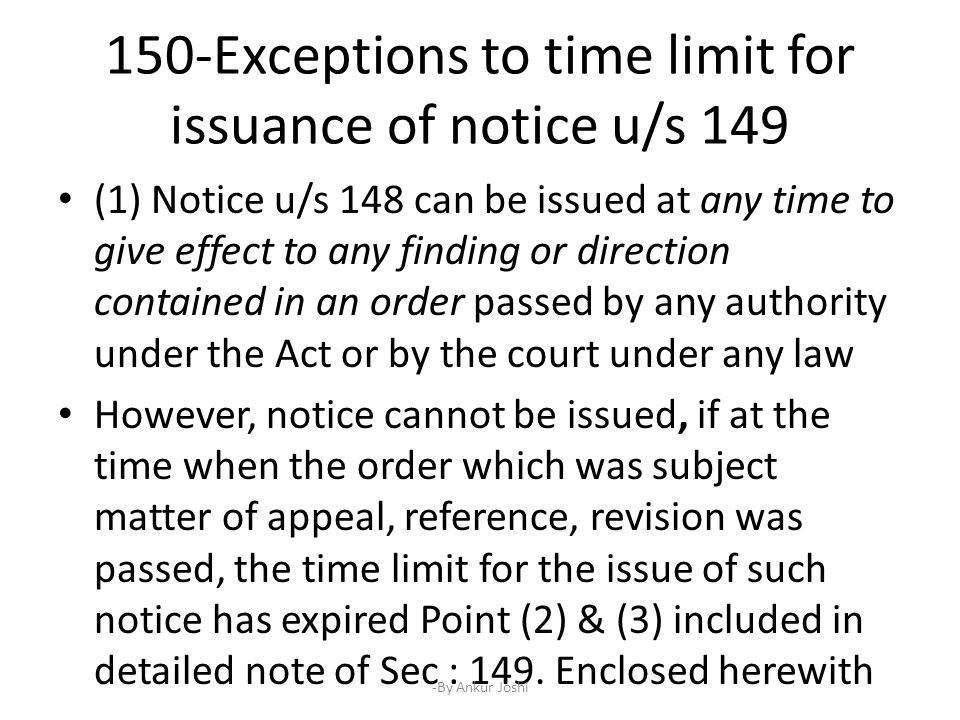

Time limit for notice u/s.148

Time limit for issuing a notice u/s.148 for reassessment or re-opening is contained in Section 149 that varies from 4 years (if the escaped assessment is less than lac) to 6 years (if the escaped income is greater than 1 lac). This is based on the amendment made by the india Finance Act, 2001. If the escaped income is related to any type of asset located outside India, the time period for issuing a notice is 16 years.

Few steps that describe the whole process of assessment/reassessment notice

- Examination of information by assessing officer.

- A belief is made by assessing officer.

- Recording of the reason in writing.

- Issuance of notice U/S 148.

- Filing of return.

- Obtaining the copy of recorded reasons.

- Filing objections by the assessee.

- Remedy of the assessee after the disposal of the assesse’s objection by assessing officer.

- Reassessment proceedings.

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income