Life Insurance Policy Payouts – Are they Taxable or Not?

Life Insurance Policy Payouts - Are they Taxable or Not?

The basic idea about life insurance policies is that they are tax-free. But this might be subject to conditions and/or exceptions. In order to utilize the benefit of tax advantage, one should be well-versed and aware of whether these proceeds are tax-free or not. So, let us have a look at how the payouts of life insurance policies are treated.

Kindly note that pension policies which have an element of life insurance are treated differently and hence are not discussed here.

Section 10(10)D of the Income Tax Act, 1961

According to Section 10(10D) of the Income Tax Act, 1961 the sum assured along with any bonus (policy proceeds) that are paid on either maturity or surrender of the policy or on the death of the person insured are totally tax-free for the receiver subject to specific conditions.

The proceeds of the policy will be taxable to the insured in certain situations:

- U/s 10(10D), any life insurance policy which has been issued post 1.4.2003 but on or before 31.3.2012, if the premium that is payable in any year goes beyond 20% of the original sum assured, the proceeds of that policy will be taxable for the insured. “Actual sum assured” refers to the amount assured that is the least in all years of the policy and it is not inclusive of any bonus amount which will be obtained over and above the assured sum. The ‘actual sum assured’ does not include premiums that have to be returned back to the policyholder.

- For insurance policies that are issued either on or post 1.4.2012, the 20% limit mentioned above has been reduced to 10%. If the insured suffers from disease or disability as mentioned by the IT Act and their policy had been issued on or post 1.4.2013, then for this person the 10% limit will be raise. However, the disability must be one of those which has been listed in section 80U (autism, mental retardation) and disease must be one of those listed in section 80DDB read with Income tax Rule 11DD (blindness).

- In case the premium which has to be paid in any year goes beyond the percentage prescribed i.e. 10%, 15% or 20% of the actual sum assured, then the entire policy proceeds would be taxed in the year of receipt. However, if the insured dies in the year where the premium crosses the prescribed percentage of the actual sum assured, the proceeds received by the nominees will be tax-free.

Note that the proceeds of a Keyman insurance policy are not tax-free according to section 10(10D) of the Income Tax Act.

Will TDS be applicable towards the payment of proceeds of life insurance policy?

According to section 194DA of the Income Tax Act, 1961, if an insured Indian resident receives any sum from an insurer under a life insurance policy, TDS @ 2% will be applicable on it, if the mentioned amount is not exempt u/s 10(10D). Also, even if these proceeds are taxable u/s 10(10D) but they do not go beyond Rs 100,000, then no TDS will be deducted by the insurer when the payment is made to the insured.

You must be aware that submission of PAN to the insurer is a must, else the TDS rate will be 20% rather than 2% in cases wherever TDS is applicable.

Also, the tax treatment of life insurance policies which have been purchased from foreign insurers (who are not registered in India) might have certain additional conditions which might differ from case to case.

Insurance is a Practical Business Investment

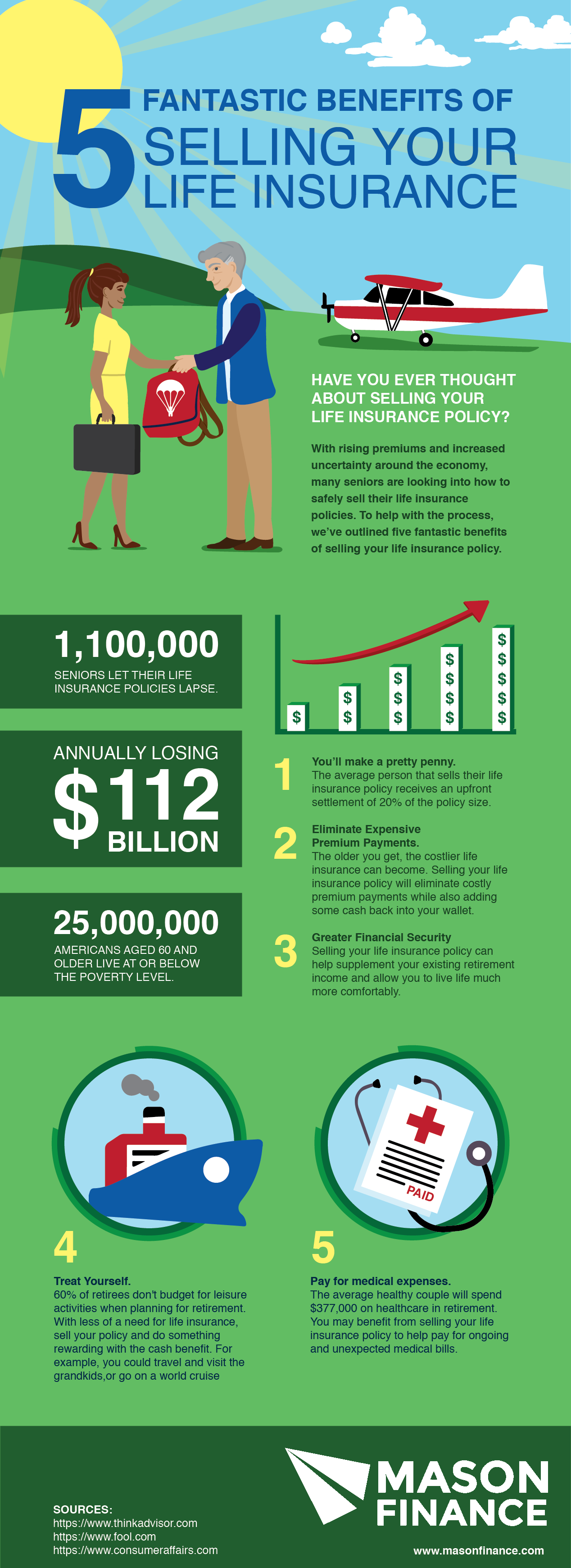

Insurance is a Practical Business Investment  5 fantastic benefits of selling your life insurance

5 fantastic benefits of selling your life insurance  Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?

Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?  Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you

Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you  Life Insurance Policies – Are they really bliss?

Life Insurance Policies – Are they really bliss?  What Insurance Companies do not tell you before selling Endowment Policies

What Insurance Companies do not tell you before selling Endowment Policies  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?