What Insurance Companies do not tell you before selling Endowment Policies

what insurance companies hide from you

An Endowment Policy is basically a life insurance contract made between the insurer and the insured which not only covers the life of the insured one but also paves the way for the policyholder to save a predetermined amount of money regularly over a specific period of time, so that he can be able to withdraw a lump sum amount on the maturity of the policy in case he survives the policy term. In case of his death before the maturity date, the nominee of the insurance is entitled to get an assured sum.

Though endowment may seem to be a risk-free insurance plan with a high level of returns. But if assessed carefully with the profit margin measures, then we can discover a number of drawbacks associated with it. Beginning with the premium, a basic endowment plan requires much more amount to be submitted regularly in comparison to a traditional term insurance plans and whole life policies.

Endowment Policies can give you as low returns as 4%. Take a careful look before opting for such policies

Endowment Plans not as rosy as they may look- If we take a close watch to the roll-over process of an endowment policy, with an example then we would understand the shortcomings of this plan in an elaborate manner. Let’s say, a person has opted for an endowment policy precisely for 30 years with annual premium ranging at Rs. 31,000. Sum assured (in case of death of the policyholder before maturity) is 10 lakhs and the calculated withdrawal amount of the same in normal maturity (applicable only if the policyholder survived the tenure) is Rs. 23,10,000.

So for 30 years if the regular premium is paid without any interruptions, then the collective total paid amount will be Rs. 9,30,000 (i.e: 31000X30=9,30,000).

Now, in endowment policies, the maturity amount is rolled over in the below-mentioned formula:

p * [{(1+r) ^ n1}/r] * (1+r)

Where, p is the amount paid per year as premium, n is number of years (i.e. 30 in this case) and r is rate of interest

Now, if we put the above-mentioned values in this formula, it will result into

31,000 * [{(1+r) ^ 30 – 1}/ r] * (1+r) = 23,10,000

Endowment Plans give pathetic Returns-Now if we analyze the policy rate of endowment plans closely, then we would get to know that this type of insurance only offers a 5.4% rate of interest only, which is pretty low in the current broader context of Indian economic. Whereas fixed deposits offer a shiny 9% rate of interest, mutual funds also give you a return of 10-12%, PPF also offers an interest of 8% and then there are ‘n’ number of products and secured investment plans are available in the market which brings on much higher and captive returns than a bounded endowment policy as Indian economy has turned into a matured macrocosmic estate with booming numbers of global tie-ups in each and every field.

Therefore, while choosing a long-term investment plan be extra careful and try to avoid plans like endowment and other alike policies. Well, if you are determined to buy a life insurance contract then it’s better to opt for a combined policy providing investment and insurance at the same time. It will definitely turn your hard earned money into a better solution for the deliberate cause which you have desired on a long run.

Life Insurance Policy Payouts – Are they Taxable or Not?

Life Insurance Policy Payouts – Are they Taxable or Not?  Insurance is a Practical Business Investment

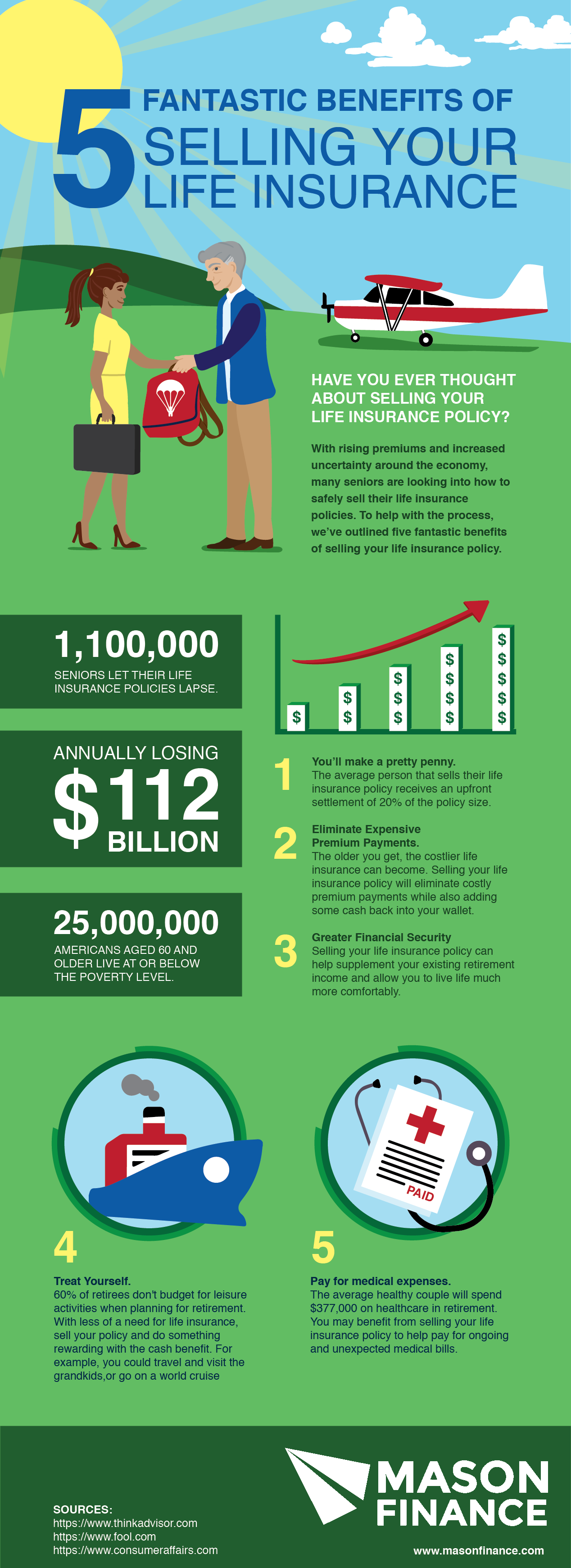

Insurance is a Practical Business Investment  5 fantastic benefits of selling your life insurance

5 fantastic benefits of selling your life insurance  Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?

Money Back Rules for Lapsed LIC Insurance Policies. What if Insurance Policy has elapsed?  Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you

Term Insurance, Accidental Death and Dismemberment or Term Insurance- Which Insurance is Best for you  Life Insurance Policies – Are they really bliss?

Life Insurance Policies – Are they really bliss?  ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?