Guide to the law on revision of assessments

According to section 263 of the Income Tax Act 1961, the commissioner has the power to call for and scrutinize the records of certain proceedings under the Income Tax Act and revise the order if the order was mistaken and detrimental to the interests of the revenue.

Guide to the law on revision of assessments

Such conferred powers of the commissioner are wide and have been subject to logical checks and balances to prevent the illogical use of such powers. The law pertaining to section 263 of the Income Tax Act 1961 has been broadly laid down by the legal authorities in many of the decisions in connection with various petitions.

Such conferred powers of the commissioner are wide and have been subject to logical checks and balances to prevent the illogical use of such powers. The law pertaining to section 263 of the Income Tax Act 1961 has been broadly laid down by the legal authorities in many of the decisions in connection with various petitions.

The following paragraphs will take you through the eligibility, the time frame and the procedures for revising the returns.

Eligibility to file the Revision of Income Tax return

In the case of any realization of the fact that you have submitted the income or deduction after filing the income tax return (ITR) for the prior fiscal, you have the opportunity of filing a revised return. This option can be exercised only if you have filed the original return before the due date 31, July.

If any error or wrong declaration is found in the original return, you have the option to file Income Tax Return with the required modifications. We can see some of the normal transactions as examples for better clarity of provisions.

Making Changes After Filing

You have the freedom to submit a revised IT return citing the changes if you have missed out to add certain amount received as interest against your savings deposit or failed to claim tax benefit for donations made to some charity organizations under section 80G of the IT Act.

The revised return can be filed before the expiration of 12 months from the end of the pertinent assessment year or before the completion of assessment by the IT department whichever is earlier. For example, if the returns have been filed for FY 2013-’14 before the due date and you need to do some changes in the returns already filed; you can file a revised return March 31, 2016. Suppose the IT department has already completed the assessment, in such cases you cannot file revised IT return.

It is suggested to check the IT return documents thoroughly even after submission and file a revised return at the earliest to avoid any penalty or interest.

How to File a Revised Income Tax Return

Online and offline options are available for filing the revised returns. But the revised returns filed online can only be revised online and those done offline return can be revised offline only. The acknowledgement number and date of filing the original return are required for revising the return.

The procedure for revising an online return is to login into IT department website, open the Excel original IT return file, enable the macros and select the options for revision of return. The next step is to select 139(5) instead of 139(1) for making changes. The acknowledgement number and date of original IT return must be mentioned at the time of effecting your changes in the file. After making the necessary changes in the file, click on “Compute Tax” and generate an XML file by validating each and every sheet and upload the file. Now the IT return revised filing is complete.

The next step is to download the revised ITR-V or acknowledgement and sign on it. Both the original as well as the revised as the ITR-V has to be sent by speed or ordinary post to the Central Processing Centre at Bangalore. You can submit the revised IT files any number of times without restrictions as long as the revision is done within the stipulated time frame. Only the most recent revised return will be considered and substituted with all the previous revised returns and the original return.

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

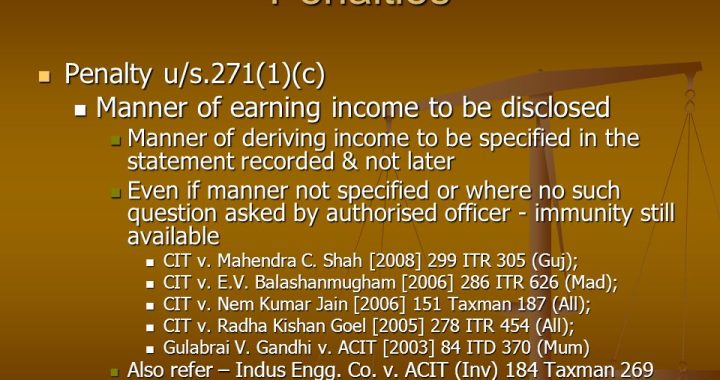

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income  Bombay High Court Upholds Section 271(1)(c) Penalty for Deliberate Non-Disclosure

Bombay High Court Upholds Section 271(1)(c) Penalty for Deliberate Non-Disclosure