What are the major differences between Fixed Maturity Plans And Fixed Deposits? Where should you invest your money?

Fixed Maturity Plans vs fixed deposits, which one is more rewarding option as Investment

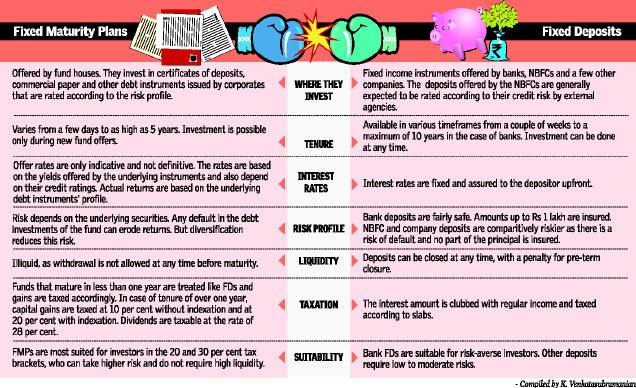

Fixed Maturity Plans or FMPs are the fixed deposits or FDs of the mutual fund industry. The investors who are pretty aware of smart investment and their profits often replace Fixed deposits with Fixed Maturity Plans . There are some basic reasons which make Fixed Maturity Plan more appealing than the fixed deposits. When it is Fixed Maturity Plans vs fixed deposits, it is the Fixed Maturity Plans which always wins.

Where to Invest?- Fixed Maturity Plans or Fixed Deposited- The basic factors of consideration

Whenever we invest, we invest for the purpose of getting higher returns. When it comes to returns, Fixed Maturity Plan vs fixed deposit always sees a clear winner in Fixed Maturity Plans.

Fixed deposits offer assured returns, which are made clear to the investor right at the point of time they invest the money. On the other hand, Fixed Maturity Plans are close-ended debt funds and the investments in them have a maturity that will coincide with the maturity of the Fixed Maturity Plans.

This is the reason why they are called Fixed Maturity plans. The yields in case of Fixed Maturity Plans are of fluctuating nature as there are chances of the actual returns deviating from the returns which were mentioned at the time of investing. This change may be a loss sometimes but often it has been seen, that there are huge profits.

Taxation of Fixed Maturity Plans and for Fixed Deposits

When it comes to taxation, then also there is a huge debate pertaining to Fixed Maturity Plans vs fixed deposit. In case of fixed deposit, the income from the interest is added to the income from the investor and it also taxable with the applicable tax deductions.

This is known as the marginal rate of tax. With Fixed Maturity Plans, the tax implication always depends upon the investment option that is whether one has gone for dividend or growth.

Returns and tenure of Fixed Maturity Plans

When the dividend option is chosen, the investors have to bear the dividend distribution tax or the DDT. In case of the growth option, the returns which are earned are treated as capital gains. They can be of short term or long term nature depending on the time period for which the investment is done.

When it comes to short-term capital gains i.e. for investments less than 365 days, the income from the investors gets added to the interest income. They are also taxed at the marginal rate of tax. In case if it is more than 365 days, the tax liability is calculated based on the lower of with indexation and without indexation.

With the indexation, Fixed Maturity Plans are always more beneficial than the Fixed deposits. In case of fixed deposit, it scores more than Fixed Maturity Plan in terms of liquidity as they can be withdrawn without any penalty.

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income