Are you filing your tax in the right way- A quick guide to the basic parts of the Income Tax Act

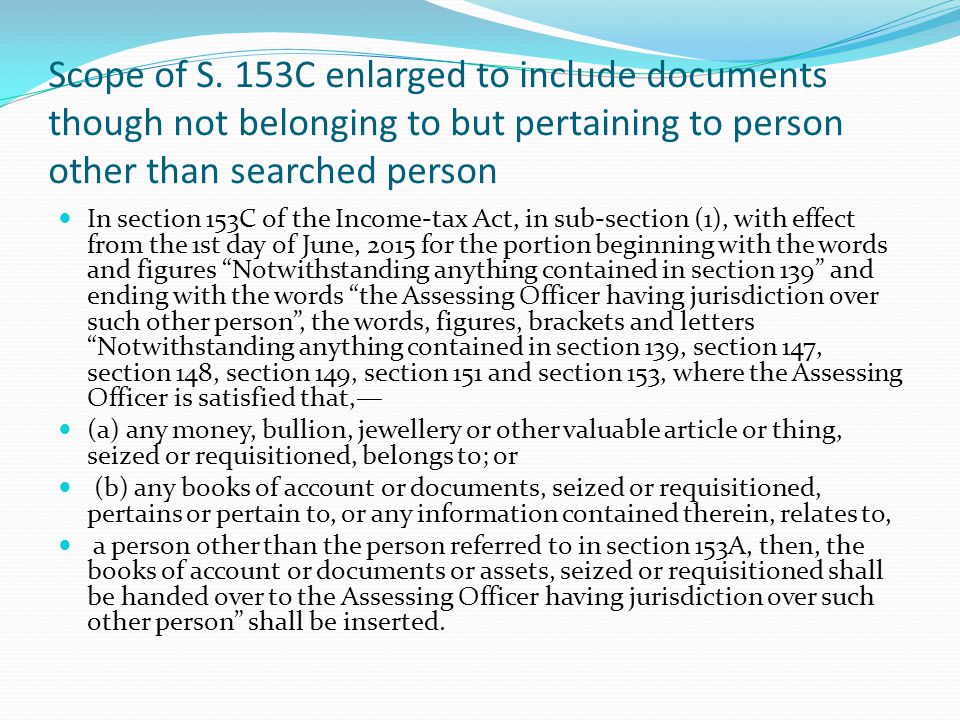

In section 153C of the Income-tax Act, in sub-section (1), with effect from the 1st day of June, 2015 for the portion beginning with the words and figures Notwithstanding anything contained in section 139 and ending with the words the Assessing Officer having jurisdiction over such other person , the words, figures, brackets and letters Notwithstanding anything contained in section 139, section 147, section 148, section 149, section 151 and section 153, where the Assessing Officer is satisfied that,— (a) any money, bullion, jewellery or other valuable article or thing, seized or requisitioned, belongs to; or. (b) any books of account or documents, seized or requisitioned, pertains or pertain to, or any information contained therein, relates to, a person other than the person referred to in section 153A, then, the books of account or documents or assets, seized or requisitioned shall be handed over to the Assessing Officer having jurisdiction over such other person shall be inserted.

Filing your income tax returns can be a tricky business. This is why there are CAs and audit firms to help you out. But this doesn’t mean that you should not hold the knowledge of the basic sections and sub-sections. Having some basic information will let you convey your returns without getting scammed. So, keeping in mind your benefit, two important parts of the Income Tax Act– one that deals with the source of unexplained expenditure and the other that sets rules on the income of any other person, have been explained below.

Section 69C

The Section 69C of the Income Tax Act mainly refers to the source of the expenditure, but not the expenditure itself. Moreover, it says that in the absence of any material found during the search, it is not justifiable to add expenditure in a block assessment.

Section 153C

The Section 153C of the Income Tax Act, states that the assessment of the income of any person other than the one in whose case the search has been initiated or the book of account, or other documents or assets have been requisitioned.

The provision of Section 153C

The sub-section (1) of Section enlists the provision of the Section 153C, which states: Notwithstanding anything that is contained in Section 139, Section 147, Section 148, Section 149, Section 151 and Section 153, the Assessing Officer must be satisfied with the requisitioned or seized money, bullion, jewelry or other valuable articles or things or book of accounts or documents belong to any person who isn’t the same person as mentioned in Section 153A. Once the Assessing Officer is satisfied that with the person’s identity, the Assessing Officer has jurisdiction over such other person and the Assessing Officer will proceed against each such other person and issue notice against them to assess or reassess income of such other person as per the Section 153A.

CIT vs. Lavanya Land Pvt. Ltd. (Bombay High Court)

In the ruling of CIT vs. Lavanya Land Pvt. Ltd. the Bombay High Court shed some light on the Section 69C and Section 153C of the Income Tax Act and arrived at a decision.

- The Tribunal considered the merits at great length, by Section 69C and finally arrived at a conclusion. The Tribunal said that merely on the strength of the alleged admission of Dilip Dherai the additions could not have been made. The Tribunal further concluded that the allegations the authority made are not at all supported by actual cash passing hands. It said that the entire decision has been based on seized documents and there was no material that was referred which would help to get to a conclusion, showing that huge amounts which were revealed from the seized documents actually transferred from one side to another. Thus the Tribunal found that the additions cannot be sustained on legal issue as well as the merits.

- Since the Tribunal negated the allegations by referring Section 69C, based on pure merits and facts, Section 153C had no place for invocation.

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar

ITAT Amritsar: No Section 269SS Violation for One-Time Cash Payment Before Sub-Registrar  Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption

Tax Officials Unleash Digital Dragnet: How New Raid Powers Redefine Privacy, Property Rights in India and likely to Fuel Corruption  Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide

Income Tax Department Rewards for Reporting Tax Evasion: A Comprehensive Guide  Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income