Create HUF to save tax and Other Important Aspects of HUF Under Income Tax, 1961

HUF-as-tax-Saving-Tool

Hindu Undivided Family (‘HUF’) is treated as a ‘person’ under section 2(31) of the Income-tax Act, 1961 (herein after referred to as ‘the Act’). HUF is a separate entity for the purpose of assessment under the Act. Under Hindu Law, an HUF is a family which consists of all persons lineally descended from a common ancestor and includes their wives and unmarried daughters. An HUF cannot be created under a contract, it is created automatically in a Hindu Family. Jain and Sikh families even though are not governed by the Hindu Law, but they are treated as HUF under the Act.

In this article, I am covering some important points related to HUF, its taxability and its assessments alongwith format of HUF creation deed.

Key points in creation of HUF and format of deed for creation of HUF

1. Under the Income Tax Act, an HUF is a separate entity for the purpose of income tax return.

2. The same tax slabs are applicable to HUF as to individual assessee.

3. You can not transfer your own assets/money into HUF.

4. If you have ancestral property and earning some income from this property, then it is better to transfer this asset to HUF and save tax up to exemption limit applicable to individual.

5. You can transfer the money received on sale of ancestral property /assets into your HUF.

6. The income from property of HUF can be further invested in instruments such as shares, mutual funds, etc. and will be assessed under HUF.

7. Existence of property or multiple members is not a pre-requisite to create HUF. A family which does not own any property may still have the character of Hindu joint family. This jointness is understood in terms of faith and food. This is because as a Hindu is born as a member of the joint family.

8. Any gifts received by the members of HUF (birthday, marriage, etc.) can be treated as assets of HUF.

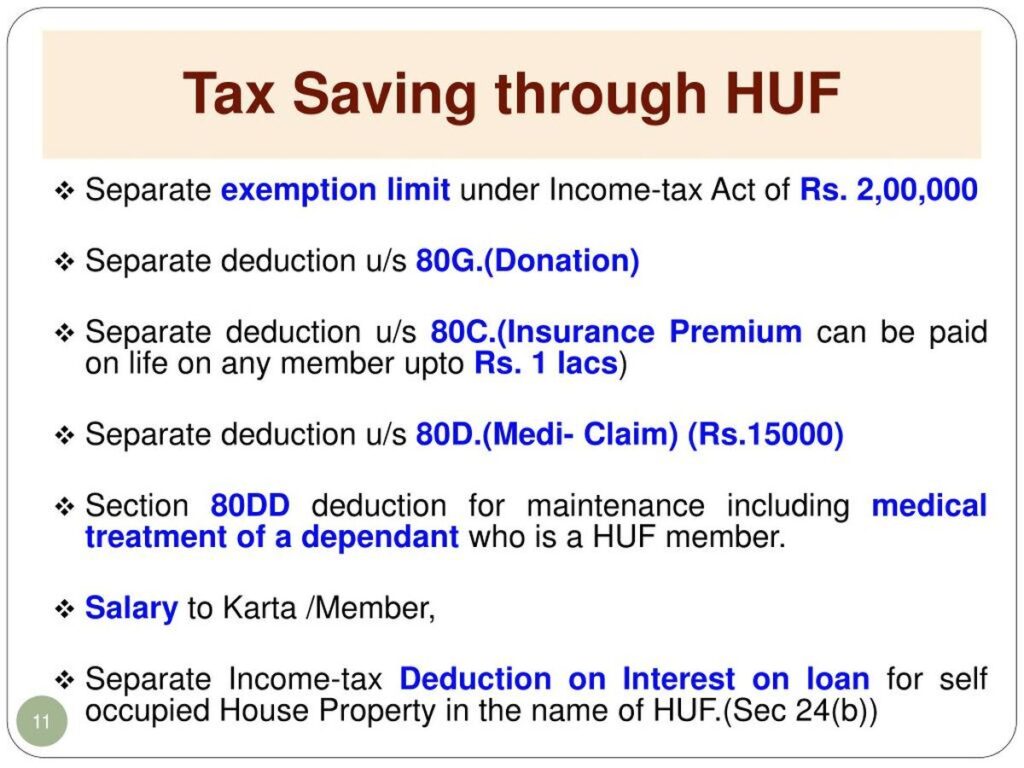

9. The HUF is taxable as separate person under income tax hence one can save tax from basic exemption of Rs. 2.5 lakh. HUF will also gain from the tax slab structure of computing income tax.

10. Apart from basic exemption of Rs. 2.50 lakh, section 80C deduction up to Rs. 1.50 lakh is also available.

11. For example, if you are in 30% tax bracket, then approx tax saving by creating an HUF will be as follows:

- Basic exemption up to Rs. 2,50,000 = nil

- Rs. 2,50,000-5,00,000 @5% = Rs. 25,000

- Rs. 5,00,000-10,00,000 @20% = Rs. 1,00,000

- 80C deductions Rs. 1,50,000

- Therefore total tax payable for HUF on income of Rs. 6,50,000 is only Rs. 12,500.

- If this income of Rs. 6,50,000 is taxed in individual hand @ 30% tax due is Rs. 1,95,000.

- Hence, you can save a total of Rs. 1,82,500 by creating an HUF and transferring ancestral property income and other income under HUF.

Note: An HUF is liable to pay Alternate Minimum Tax if the tax payable is less than 18.5 per cent (including cess and surcharge) of “Adjusted Total Income” subject to prescribed conditions.

12. The following incomes are not taxed as income of HUF:-

- If a member has converted or transferred without adequate considerationhis self-acquired property into join family property, income from such property is not taxable in hands of the family.

- Income of impartible estate (though it belongs to family) is taxable in the hands of holder of estate and not in hands of HUF.

- Personal income of the members cannot be treated as income of HUF.

- “Stridhan” is absolute property of a woman, hence income arising therefrom is not taxable as income of HUF.

- Income from individual property of daughter is not taxable in hands of HUF even if such property is vested into HUF by daughter.

13. An HUF is recognized as a separate assessable entity under the Act. Its income may be assessed if following two conditions are satisfied:

- There should be a coparcenership. In this connection, it is worthwhile to mention that once a joint family income is assessed as that of HUF, it continues to be assessed as such in subsequent assessment years till partition is claimed by coparceners.

- There should be a joint family property which consists of ancestral property, property acquired with the aid of ancestral property and property transferred by its members.

Please note that Property obtained by daughter from joint family property would be her absolute property. Any income therefrom is chargeable to tax in her hands in the individual status only. This will also apply to any legal heir obtaining property in the capacity of a descendant.

FORMAT- II

[To be executed on Rs. 200 Stamp Paper in Maharashtra]

DECLARATION OF GIFT MADE BY ________________________

TO THE HINDU UNDIVIDED FAMILY OF ___________________

I, _____________________________, residing at _______________________ ____________________________________________________________, do hereby declare and affirm as under:

- That out of natural love and affection borne by me towards the Hindu Undivided Family of ______________________________, I have made a gift of Rs.______ (Rupees _________________ only) as per the following details:

By Cheque No.________, dated __________, drawn on Bank ____________________, ________________ Branch, in favour of ________________________ HUF.

- The above Gift has been duly accepted by ________________________, as Karta of his Hindu Undivided Family and has been duly acknowledged hereunder.

- This Declaration of Gift is made to record the fact that I have made this Gift in favour of the Donee as above, who now has the absolute right, title and interest in the gifted amount.

Date: _____, 200 _____

(Signature of the Donor)

ACKNOWLEDGEMENT OF GIFT

I, ________________________, hereby acknowledge having received the above gift made to my Hindu Undivided Family by _________________________.

Date: ___________, 200__ ___________________

(Signature of the Donee

as Karta of his HUF)

A. Partition of HUF under Income Tax Act, 1961 and its assessment after Partition.

The Partition of HUF should be recognized as per the Income Tax Act and not as per the Hindu Law. Section 6 of the Hindu Succession Act would govern the rights of the parties but insofar as income-tax law is concerned, the matter has to be governed by section 171(1) of the Income Tax Act, 1961 [Add. CIT v. Maharani Raj Laxmi Devi [1997] 091 Taxman 020 (SC)]. The Hindu Law does not require that the property in every case be partitioned by metes and bound or physically into different portions to complete a partition. But the Income Tax Law introduced certain additional conditions of its own to give effect to the partition u/s 171.

Section 171 of the Income Tax Act, 1961 defines the partition of HUF and deals with the provisions of assessment after its partition. Thus a transaction may be treated as severance of status under Hindu Law but not a partition under 1961 Act as physical division of property is necessary under 1961 Act

Q1. What is the Partition of HUF?

• The Partition of HUF can be categorized as under:-

- Partial Partition –

Partial partition means a partition which is partial as regards the persons constituting the HUF, or the properties belonging to the HUF, or both.

2. Total or Complete Partition –

Assets of HUF are physically divided. As per explanation to section 171 of the Income Tax Act,

‘Partition’ means

(i) where the property admits of a physical division, a physical division of the property, but a physical division of the income without a physical division of the property producing the income shall not be deemed to be a partition; or

(ii) where the property does not admit of a physical division, then such division as the property admits of, but a mere severance of status shall not be deemed to be a partition.

Therefore a transaction can be recorded as a partition u/s 171 only if, where the property admits of a physical division, such division has actually taken place.

Q2. What is the tax implication of Partial Partition of HUF?

A Partial partition taken place after 31-12-1 978 is not recognized the Income Tax Act, 1961 (Sub-section 9 of section 179. Therefore even after the Partial partition, the income of the HUF shall be liable to be assessed under the Income-Tax Act as if no partition had taken place.

Q3. What is the tax Implication of Full Partition of HUF?

After the Partition, the assessment of HUF shall be made as per the provisions of Section 171 of the Income Tax Act and order to be passed by the Assessing Officer.

Q4. What is the procedure of partition and assessment after partition of HUF under Income Tax Act

The following procedure u/s 171 is prescribed under the Income Tax Act regarding partition and assessment after partition of HUF:

- The HUF hitherto assessed as undivided shall be deemed for the purposes of this Act to continue to be a Hindu undivided family, except where and in so far as a finding of partition has been given under this section in respect of the HUF.

- Where, at the time of making an assessment u/s 143 or u/s 144, it is claimed by or on behalf of any member of a Hindu family assessed as undivided that a partition, whether total or partial, has taken place among the members of such family, the AO shall make an inquiry thereinto after giving notice of the inquiry to all the members of the family.

- On the completion of the inquiry, the AO shall record a finding as to whether there has been a total or partial partition of the joint family property, and, if there has been such a partition, the date on which it has taken place.

- Where a finding of total or partial partition has been recorded by the AO and the partition took place during the previous year,—

(i) the total income of the joint family in respect of the period up to the date of partition shall be assessed as if no partition had taken place; and

(ii) each member or group of members shall, in addition to any tax for which he or it may be separately liable and notwithstanding anything contained in clause (2) of section 10, be jointly and severally liable for the tax on the income so assessed.

- Where a finding of total or partial partition has been recorded by the AO and the partition took place after the expiry of the previous year, the total income of the previous year of the joint family shall be assessed as if no partition had taken place; and each member of group of members shall be jointly and severally liable for the tax on the income so assessed.

- Notwithstanding anything contained in this section, if the AO finds after completion of the assessment of a Hindu undivided family that the family has already effected a partition, whether total or partial, the AO shall proceed to recover the tax from every person who was a member of the family before the partition, and every such person shall be jointly and severally liable for the tax on the income so assessed.

- For the purposes of this section, the several liability of any member or group of members thereunder shall be computed according to the portion of the joint family property allotted to him or it at the partition, whether total or partial.

- The above provisions shall, so far as may be, apply in relation to the levy and collection of any penalty, interest, fine or other sum in respect of any period up to date of the partition, whether total or partial, of a HUF as they apply in relation to the levy and collection of tax in respect of any such period.

Q5. Whether the sum received by a member as and towards his share as coparcener of HUF, on its partition is taxable as income?

The sum received by a member as and towards his share as coparcener of HUF, on its partition cannot be brought to tax as income [Smt. Sudha V. Iyer v. ITO 15 taxmann.com 234 (ITAT-Mum.) [2011]

Q6. Whether setting apart of certain assets of HUF in favour of certain coparceners on a condition that no further claim in properties will be made by them, is a partition under Income Tax Act?

Setting apart of certain assets of HUF in favour of certain coparceners on the condition that no further claim in properties will be made by them, is nothing but a partial partition and not a family arrangement and not recognised in view of section 171(9) of the Act. [ITO v. P. Shankaraiah Yadav 91 ITD 228 (2004) (ITAT-Hyd.)].

Q7. Whether there is an ipso facto partition of joint family properties immediately after the death of a male coparcener having coparcenary interest in coparcenary property?

The gist of the various pronouncements of the Hon’ble Supreme Court is that there is no ipso facto partition of joint Hindu family properties immediately after the death of a male coparcener of the Mitakshara school having coparcenary interest in the coparcenary property. The fiction given by Explanation 1 to section 6 of 1956 Act has nothing to do with the actual disruption of the status of a HUF. It freezes or quantifies the share of a female heir in the coparcenary property on account of the death of a coparcener at the relevant point of time.

Therefore, there was no partition and disruption of the HUF as per Explanation 1 to section 6 of the 1956 Act, in the instant case.

Q1 What is the residential status of the HUF under Income Tax Act?

Section 6(2) of the Income-tax Act, 1961, clearly contemplates a situation where a HUF can be non-resident also. In fact, HUF can also be Not Ordinarily Resident.

HUF will be considered to be resident in India unless, during the previous year, the control and management of its affairs is situated wholly outside India. In such a case, it will be treated as non-resident HUF.

Section 6(6)(b) of the Income-tax Act, 1961 further provides that, in case of a HUF whose manager has not been resident in India in nine out of ten previous years preceding the previous year or has, during the seven previous years preceding that year, been in India for a total 729 days or less, such HUF is to be regarded as not-ordinarily resident within the meaning of the Income-tax Act, 1961. As such, it is not necessary for a HUF to be resident in India.

Q2. How the residential status of the HUF can be determined in case of change of Karta of HUF during the relevant year?

In case of change of Karta of HUF during the year, the residential status of HUF can be determined by considering the period of stay in India of both Karta of HUF i.e. previous Karta and successive Karta.

Q3. Whether different residential status for HUF is possible for different years?

Under the Income Tax Act the residential status is determined with reference to the previous year relevant to a particular assessment year. Therefore the residential status of HUF may also be different for different assessment years considering the facts of relevant previous year.

Q4. Whether the non-residential status of Karta would alter the residential status of HUF?

As discussed in the earlier answer, the test is not where the Karta resides; the test is where the control and management of the affairs of HUF is situated. Even if a part of control and management is situated in India, such HUF will be treated as resident in India.

Though, generally, Karta is supposed to manage the affairs of HUF, it is not an absolute rule and, by consent, the power of control and management may be delegated to other members of the family, either fully or partially.

The relevant factor for determining the status is where the control and management of HUF is situated (even in part). Therefore the HUF may be resident even where the Karta was residing outside India for whole of the year.

Q5. Whether the income received by members from HUF is taxable?

As per Section 10(2) of the Income-tax Act, 1961, any sum received by an individual from Hindu Undivided Family of which he is member is exempt from tax.

But the amount received not as a member of Joint Family but in pursuance of some statutory provision, etc. would not be exempted in this section. Also the position of member of joint family in law to claim the right u/s 10(2) does not get affected only with the reason that they are living apart from the other members of the family.

C. Taxability of Income from house property in the name of HUF

1. Self occupied one Residential House & the tax gain specially by way of Interest on Loan & Repayment of Loan

2. Special 30% deduction on Rental Income also to HUF.

3. Exemption from Wealth-tax the real estate of HUF – One House Wealth Tax Free (Commercial / Rented Residential)

Q1. Whether the Property purchased with the joint fund is assessed in the hands of HUF only?

Property purchased with the aid of joint family funds, howsoever small that may be, still the property would be HUF income and cannot be income of the individual with major portion of purchase price.

The Hon’ble Madras High Court has held in the case of S. Periannan v. CIT (1991) 191 ITR 278, that

“When once the estate had become the property of the assessee-Hindu undivided family on its coming into existence, there could be no change in its character by reason of the fact that, subsequently, in the books of the assessee-Hindu undivided family, the account of Sathappa Chettiar was debited with the amount which have been drawn for the purchase of the estate. In these circumstances. The Tribunal rightly held that the Grove Estate should be considered as belonging to the assessee-Hindu undivided family.”

Q2. Whether the Income from House property to be charged in the hands of HUF only where property is purchased in the name of HUF?

In the case of ACIT vs. Rakesh S. Agrawal [2010] 36 SOT 148 (AHD.) it was held that:

AO found that the assessee had purchased a house property from ‘A’. The assessee’s case was that since the investment was made in the name of HUF, it was not declared in his individual return. The AO, however, took a view that the funds for acquiring the property in question were met from the personal sources of the assessee. He thus determined annual letting value of the property resulting in certain addition to the assessee’s income. On appeal, the Commissioner (Appeals) directed the AO to consider the annual letting value of the property in the hands of HUF and deleted the impugned addition.

D. Proprietorship and Partnership by HUF

Q1. Whether HUF can do a business in its own name?

- HUF can be a Proprietor of one or more than one Business concerns.

- Separate name can be kept of HUF business entity.

- No tax Audit of HUF business if Turnover within Rs. 1 crore (F.Y. 201 2-1 3).

- Business Income Computation @ 8% without books of account in case turnover is upto Rs. 1 crore – The Presumptive Basis

Q2. Can a Karta of HUF become partner in a firm?

The Hon’ble Supreme Court in Ram Laxman Sugar Mills vs. CIT [1967] 66 ITR 613 observed that a HUF is undoubtedly a “Person” with in the meaning of section 2(31), it is however not a juristic person for all purposes and cannot enter in to an agreement of partnership either with another HUF or Individual. It is open to the manager of a Joint Hindu family, as representing the family, to agree to become a partner with another person. And therefore any remuneration received by Karta would be the personal income of Karta and not the income of the HUF as there is no real connection between the investment of the assets of HUF and remuneration received by Karta.

Q3. Whether the amount received by Karta from partnership firm as remuneration is assessed in the hands of HUF?

The remuneration received by Karta as representative of HUF cannot be treated as income of the HUF. Remuneration will be income of HUF only when there is direct nexus between family funds and remuneration paid.

In Brij Mohan vs. CIT 201 ITR 831 (1993), the Supreme Court held that where the receipt is a compensation made for the services rendered and not for the return of investment, it is to be treated as individual income of the partner.

However, where members of HUF become the partners in a firm by investment of family funds & not because of any Special Services rendered by them, then the income will belong to HUF. {Lachman Das Bhatia & Sons vs. Commissioner of Income-tax [2007] 162 Taxman 118 (Delhi)} {D.N. Bhandarkar v. CIT 158 ITR 724 Kar (1986)}

Once the character of an individual has been treated differently than H UF for the purposes of interest, there is no reason as to why that would not extend to the salary and bonus paid to such partners on account of their personal services rendered to the firm in contra-distinction to their capacity as representatives of HUF .

Therefore, the same reasoning would apply to the cases where payment in the form of salary and bonus has been made to a partner in his individual capacity in contra-distinction to his representative character of the HUF. [CIT v. Unimax Laboratories [2007] 164 Taxman 373 (P & H)].

Q4. Whether deduction is available to partnership firm u/s 40(b) in respect of salary or commission paid to a partner who was a partner in representative capacity of HUF.

As per Section 40(b)(i)

“in the case of any firm assessable as such,—

any payment of salary, bonus, commission or remuneration, by whatever name called (hereinafter referred to as “remuneration”) to any partner who is not a working partner”

Partner of a firm is an individual even if he is partner as a representative of HUF

- Where assessee-firm paid salary to a partner who was actively engaged in conducting affairs of business of firm, it was to be held that requirement of Explanation 4 to Section 40(b) stood complied with, and, thus, assessee-firm would be entitled to deduction in respect of salary paid to said partner even though he was a partner in representative capacity of HUF. [P. Gautam & Co. vs. JCIT [2011] 14 taxmann.com 79 (Ahd.)]

- Salary paid to working partner even though as Karta of HUF, is received as individual and as working partner, hence allowable as deduction while computing income of firm. [CIT vs. Jugal Kishor & Sons [2011] 10 taxmann.com 82 (All.)]

- It is individuals of HUF who indirectly become partner in firm in which HUF is said to be partner and therefore provisions of Section 40(b) that prohibits deduction of payments of commission to any partner who is not a working partner, in computing income under the head PGBP, will not be applicable. Therefore deduction of any commission payable to any individual of HUF shall be allowable. [CIT v. Central Scientific Instrument Corporation [2010] 1 DTLONLINE 149 (All.)]

Q5. Whether the Salary income of wife of Karta is club in the Income of HUF?

Where a person is a partner in a partnership firm not in his individual capacity but as the karta of the Hindu undivided family, the income accruing to his wife on account of her being a partner in the same partnership firm cannot be included in the total income of such person in an individual assessment or in the assessment of the Hindu undivided family. [CIT v. Om Prakash [1996] 217 ITR 785 (SC) See also CIT v. Ram Krishna Tekriwal [2005] 274 ITR 266 , Satish Chand Gupta v. CIT [2007] 160 Taxman 224 (All.)].

In the case of Pratap H. Desai (HUF ) v. ACIT [2009] 118 ITD 29 (Pat.) it was held that:

Assessee was a partner in a firm which was dissolved with effect from 1-1-1999 and its business was taken over by the assessee in the capacity of a HUF – the assessee sought to set-off loss of the said firm against the profit of his business as HUF

Section 78(2) prohibits carry forward and set-off of losses of one person by another person except when the other person receives the losses by inheritance. Section 78 shows that where succession to business is by inheritance, then loss will be allowed to be set-off and not otherwise.

Therefore, assessee was not entitled to set-off of losses of firm against his individual income

E. Capital Gain Exemption available to HUF

General provisions applicable to HUF:

- Cost Inflation Index benefit available to Calculate Cost of the Asset.

- Tax benefit of 20% Tax on Long-term Capital Gains.

- Long-term Capital Gains Saving by investing in Residential Property u/s 54/ 54F.

- Exemption on sale of Agricultural land u/s 54B.

- Saving Tax on Long-term Capital Gain possible by investing in Capital Gains Bonds of NHAI / RECL u/s 54EC.

- Exemption from tax on LTCG on transfer of residential property if invested in a manufacturing small or medium enterprise u/s 54GB (introduced vide Finance Act, 2012)

Various practical aspects of taxability of Capital gain the hands of HUF are discussed as under:

Q1 To avail the benefit of adopting market value as on 1-4-1981, upto which date the capital asset should have become property of the previous owner?

Capital asset should have become property of previous owner before 1-4-1981 to make assessee entitled to benefit of adopting market value as on 1-4-1981

but where construction of building was completed in 1988 and possession of flat was handed over to previous owner, i.e., HUF, it could not be said that flat itself became property of HUF prior to that date and, hence, assessees were not entitled to adopt market value of flat as on 1-4-1981.In view of specific provisions of Explanation (iii) to section 48, indexing had to be allowed of the financial year in which flat was held by assessee on partition of HUF. [DCIT v. Kishore Kanungo 102 ITD 437 (Mum.) [2006]].

Q2. Whether the benefit u/s 54 can be available on purchase of more than one residential house Properties?

A plain reading of section 54(1) discloses that when an individual assessee or an HUF assessee sells a residential building or land appurtenant thereto, he can invest capital gain for purchase of a residential building to seek exemption of the capital gain tax. The expression ‘a residential house’ should be understood in a sense that building should be residential in nature and ‘a’ should not be understood to indicate a singular number.

That when an HUF’s residential house is sold, the capital gain should be invested for the purchase of only one residential house, is an incorrect proposition. After all, the property of the HUF is held by the members as joint tenants. If the members, keeping in view the future needs in event of separation, purchase more than one residential building, it cannot be said that the benefit of exemption is to be denied u/s 54(1).

[CIT v. D. Ananda Basappa 180 Taxman 4 (Kar.) [2009] ]

Q3. Whether to claim benefit of section 54F, residential house which is purchased or constructed has to be of same assessee whose agricultural land is sold?

To claim benefit u/s 54F, residential house which is purchased or constructed has to be of same assessee whose agricultural land is sold.

The, it is written it same view is expressed by Delhi High Court in the case of Vipin Malik (HUF) Vs CIT 183 Taxman 296 (2009), It was held that:

“The agricultural land, which was sold was of the HUF of the assessee but the flat purchased in the co-operative society was not in the name of the HUF. The flat was in the individual name of the assessee along with his mother. To claim the benefit of section 54F, the residential house which is purchased or constructed has to be of the same assessee whose agricultural land is sold and it was not the case in the instant case. [Para 9]

Clearly, therefore, there was no question of applicability of section 54F in the aforesaid facts and circumstances.”

Q4. Whether in terms of section 48, payment made by assessee for education, maintenance and marriage of his unmarried daughter, though under consent decree, could be said to be an expenditure wholly and exclusively incurred in connection with transfer of property?

Under section 48, any payment made by assessee for education, maintenance and marriage of his unmarried daughter, though under consent decree, could not be said to be an expenditure wholly and exclusively incurred in connection with transfer of property or could also not be considered as a cost of acquisition or cost of improvement.

[Krishnadas G. Parikh v. DCIT [2008] 114 ITD 362 (AHD)].

Q5. Whether the exemption u/s 54B of the IT Act is available to HUF?

Exemption under Section 54B is also available to HUF subject to the following condition:

If HUF transfer a land which is used for agricultural purposes by a HUF, the rollover relief u/s 54B is available to the HUF. The amendment is applicable on transfers made after 01-04-2013.

*Even before the amendment, exemption was being allowed to HUF.

Same view is expressed in K.S. Jain & Sons (HUF ) v. ITO 173 Taxman 114 (Delhi) (Mag.) [2008], it was Held, AO was wrong in denying deduction u/s 54B to assessee on ground that assessee being an HUF was not entitled to deduction u/s 54B.

Q6. Whether exemption from Capital Gain u/s 54GB newly introduced vide Finance Act, 2012 is available to HUF?

Exemption from tax on LTCG on transfer of residential property if invested in a manufacturing small or medium enterprise.

- Available to an Individual or HUF.

- Transfer made on or before 31st March, 2017.

- Amount is reinvested before due date of furnishing return of income u/s 139 (1)

- In Equity of a new start up SME company in the manufacturing sector in which in hold more than 50% share capital or voting rights

- Amount is utilized by the company for purchase of new plant & machinery

- The share cannot be transferred within a period of 5 years

F. Taxability of gift received in cash or in kind by HUF without consideration

1. If any sum of money exceeding Rs. 50,000 is received by the HUF without consideration then provisions of section 56(2)(vii) are applicable and the same is taxable in the hands of HUF.

2. Gift received in kind by HUF without consideration is also taxable subject to the provisions of s. 56(2)(vii).

The definition of relative provided under Explanation to Section 56(2) (vii) shall be amended by Finance Act, 2012. The amendment is as under:

The provisions of section 56 are amended so as to provide that any sum or property received without consideration or inadequate consideration by an HUF from its members would also be excluded from taxation [w.r.e.f. 1-10-2009].

For this purpose, clause (e) of the Explanation below section 56(2)(vii) is to be substituted to provide that in case of HUF, relative means members of the HUF.

After the amendment,

“(e) “relative” means,—

(i) in case of an individual—

(A) ******; and

(ii) in case of a Hindu undivided family, any member thereof.”

The amendment as above is inspired by the decision of ITAT in Vineetkumar Raghavjibhai Bhalodia v. ITO 46 SOT 97 (Rajkot-ITAT) (2011) where it was held that Gift received from HUF is gift from relative.