Can DTAA help NRIs to avoid double taxation?

If you are an NRI and are moving abroad leaving behind sources of income, you need to pay tax on such earnings in India. It will be added to your net global income and will be taxed accordingly.

If you are an NRI and are moving abroad leaving behind sources of income, you need to pay tax on such earnings in India. It will be added to your net global income and will be taxed accordingly.

One can utilize the provisions of the Double Taxation Avoidance Agreement (DTAA) to save himself from Double Taxation.

What is double taxation?

Double taxation means taxability imposed by two countries. As per global rules, if an assessee is a resident in one country but has a source of income in another one, at times his income is taxed in both the countries. In such cases, Double Taxation is said to occur.

What is DTAA?

DTAA is a tax treaty signed between nations. India has signed DTAA with many nations of the world. Such treaties can be bilateral which means only between two countries or can be multilateral which means between many countries.

Double Tax Avoidance Agreement (DTAA) is an agreement which is entered between countries to promote economic trade and investments between two nations. Such treaty can apply to two or more nations.

The rules vary with treaties. In India, the tax treaty with Mauritius provides zero tax in case of capital gains on equities. On the other hand with the United States of America, tax is imposed on capital gains.

Objects of DTAA:

The aim of DTAA is to avoid double taxation of the same income. These treaties are beneficial for individuals who reside in other countries for their work, provided such a treaty exists between their country of residence and the country where their source of income arises.

Advantages of DTAA:

The benefits of DTAA are lower rate of TDS, income tax exemption, etc.

The mechanism of using DTAA:

Double tax avoidance can be affected in the following two methods for availing Tax Benefits by using DTAA –

• Exemption Method: Resident countries allow exemptions to income earned in another country. As per this method, income is taxed in either of the two nations. According to the terms of the treaty with countries like Greece, Libya, etc. in case of a citizen, any income from dividend, income from the fees for technical services, etc. arising in India will be taxed in India. For a resident if such income arises in any of the three nations, the income will be solely taxed in the three countries and not in India.

• Tax Credit Method: It provides credits on account of the income tax paid in another country though the amount differs from country to country ranging from 15% to 30%. The income tax paid in the country where it arises is deducted from the Global income, thereafter income tax is paid then on residual amount.

Types of tax credit method:

1. Ordinary credit method;

2. Underlying Tax Credit method.

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

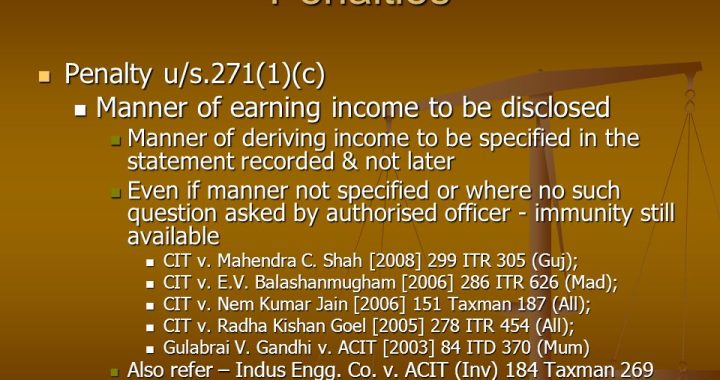

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income  Bombay High Court Upholds Section 271(1)(c) Penalty for Deliberate Non-Disclosure

Bombay High Court Upholds Section 271(1)(c) Penalty for Deliberate Non-Disclosure  Reporting of Foreign Assets by Indian Taxpayers under Section 139(1) of the Income Tax Act

Reporting of Foreign Assets by Indian Taxpayers under Section 139(1) of the Income Tax Act  Can an assessee pay House Rent to his parents and claim relief? Would there be any legal complications?

Can an assessee pay House Rent to his parents and claim relief? Would there be any legal complications?