Audited books of account of an assessee cannot be denied

In the Assistant Commissioner of Income Tax, Central Circle-1, Rajkot vs. Rushabh Vatika, IT APPEAL NO. 51 (RJT.) OF 2013 it has recently been held that audited profit and loss books of account of an assessee cannot be denied later on by him.

In the Assistant Commissioner of Income Tax, Central Circle-1, Rajkot vs. Rushabh Vatika, IT APPEAL NO. 51 (RJT.) OF 2013 it has recently been held that audited profit and loss books of account of an assessee cannot be denied later on by him.

Brief facts of the case:

The assessee had a business of real estate development. At the time of a search conducted by the tax department at the business premises as well as the residence of the assessee, materials were found relating to sale consideration of plots in cash being the impugned sum and the same was accepted by the assessee.

The assessee credited the impugned sum to its profit and loss statement which was accepted by auditor. In the return of income filed by the assessee, he first excluded the impugned sum from net profit and then added 20% thereof. The Assessing Officer levied tax upon the total sum.

In an appeal filed by the assessee, the Commissioner (Appeals) directed the Assessing Officer to apply net profit rate of 30%. The Revenue preferred an appeal before the Tribunal against the order of the Commissioner (Appeals).

Issues appearing before the Tribunal:

The issue which was raised in the appeal before the Tribunal was whether the net profit that was duly certified by tax auditor declared by the assessee in its audited profit and loss account could be discarded by the assessee without showing any evidence to substantiate that profit and loss account and audit report were incorrect.

Another issue that was raised was whether the net profit shown by the assessee in its audited profit and loss account could be decreased by 80% of the impugned sum without providing any detail to show that expenses up to 80% of the impugned sum were incurred by the assessee and the same can be allowed.

Arguments raised by the Revenue:

The revenue contended that question of applying rate of net profit did not arise as books of account were not rejected as per section 145(3), as such; the order of Commissioner (Appeals) should be set aside.

Arguments raised by the assessee:

The counsel appearing on behalf of the assessee contended that the order passed by the Commissioner (Appeals) was based on facts and the same was sustainable on merits. The claim of the assessee placed before the Tribunal was that what should be taxed is the profit embedded in the impugned sum, which according to the assessee, was merely 20%. The assessee claimed that the remaining 80% of the impugned sum was his expenditure for which he had offered only 20% thereof to tax.

The judgment:

The Tribunal held that Section 145(3) empowers the Assessing Officer to reject the books of account if he is not satisfied regarding its authenticity or where the method of accounting as per section 145(1) or accounting standards as per section 145(2) have not been properly followed by the assessee. Save and except the cases covered by section 145(3), the books of account maintained by an assessee are binding on the Assessing Officer and computation of income will be based on that. Similarly the assessees should be bound by the entries made in their books unless they can show proof of the correctness of the books of account.

It was held that an assessee cannot reject his own profit and loss account, balance sheet and its audit report.

Reference was made to section 37 of the Income Tax Act which deals with deduction of expenses incurred for the business purposes. Deduction towards expenses incurred by an assessee can be allowed only when it is proved by him that such expenses have been incurred exclusively for the purposes of business and they are not personal or capital expenditure. It should be further proved that such expenses have been incurred in the same year in which the deduction has been claimed. It was the assessee who claimed deduction of 80% of the impugned sum from net profits; as such the onus was obviously on the assessee to prove that the essentials purposes were fulfilled. The assessee failed to discharge its burden. The claim of the assessee was held to be inconsistent with the statutory provisions.

The order of the Commissioner (Appeals) was reversed and that of the Assessing Officer was restored. The appeal filed by the Revenue was allowed.

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?

Forfeiture of Gratuity by Employer- What are the Remedies for an employee- Can employer be challenged?  Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

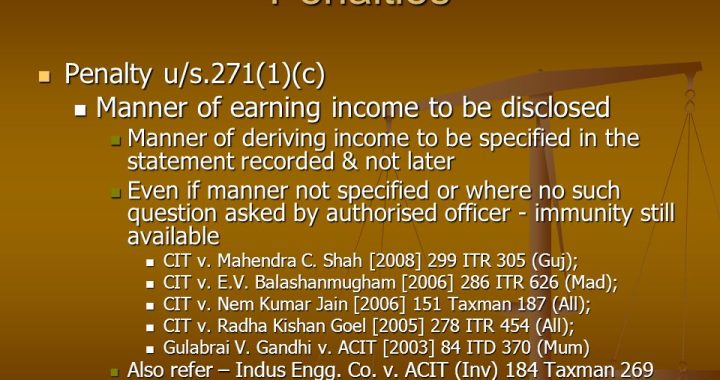

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income  Bombay High Court Upholds Section 271(1)(c) Penalty for Deliberate Non-Disclosure

Bombay High Court Upholds Section 271(1)(c) Penalty for Deliberate Non-Disclosure  Reporting of Foreign Assets by Indian Taxpayers under Section 139(1) of the Income Tax Act

Reporting of Foreign Assets by Indian Taxpayers under Section 139(1) of the Income Tax Act  Can an assessee pay House Rent to his parents and claim relief? Would there be any legal complications?

Can an assessee pay House Rent to his parents and claim relief? Would there be any legal complications?