Are the properties purchased from NRIs subjected to TDS?

Tax has to be deducted at source when someone makes payment to a NRI vendor for purchasing a property. Non-deduction of tax at source at the time of making payments to vendors can make one liable to penalties.

Tax has to be deducted at source when someone makes payment to a NRI vendor for purchasing a property. Non-deduction of tax at source at the time of making payments to vendors can make one liable to penalties.

Payments made to Non-Resident Indians:

A NRI seller is usually governed by the provisions of Section 195 of the Income Tax Act, 1961.

Provisions of section 195 of the Act:

According to the provisions of section 195 of Income Tax Act, anybody who is responsible for making a payment to a Non-Resident, provided it is not a foreign company, of any interest or any amount payable under the Act but it is not salary income, shall during credit of the income to the account of the person making such payment either in cash or by cheque or draft, deduct income tax thereon at the prevailing rate.

Rate of deduction of TDS:

Selling a property by a NRI is taxable as per section 115E of the Income Tax Act 1961. The rate of tax currently in force is 20%. A NRI has to file his or her income tax return in India for claiming the refund of any excess amount which has been deducted.

TDS needs to be deducted at the rate of 20% in addition to EC & SHEC on the consideration amount. Moreover a surcharge at the rate of 10% will be applicable if the consideration is more than Rs. 1 crore.

What is the prescribed time of deducting TDS?

Tax shall be deducted while making the payment or at the time of giving credit to the vendor, whichever happens earlier. If any earnest money is paid, then TDS needs to be deducted while making the advance payment.

In case of payment through installments, TDS needs to be deducted at the time of paying every installment. The tax deducted is paid to the credit of Central Government within seven days from the end of the month in which the deduction is made.

Issuance of TDS certificate:

When tax is deducted at source, a TDS receipt should be issued showing the amount of tax which is withheld. Such receipts can only be issued by entities having a Tax Deduction Account number (TAN). The purchaser has to apply for and get a TAN from the department; thereafter he can issue a TDS receipt to the vendor for the withheld TDS. After the purchaser deducts the TDS and issues a receipt, he is responsible to submit the same to the tax authority.

Is such deduction mandatory?

It is clearly stated in the Act that whether the vendor has any long term capital gain or short term capital gain or even no gain, the purchaser is bound to deduct TDS on the consideration. The person purchasing the property from a NRI has to deduct TDS from the total consideration and not on the profit before making such payment to the NRI.

Employer can forfeit gratuity of an employee in case of moral turpitude

Employer can forfeit gratuity of an employee in case of moral turpitude  Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income

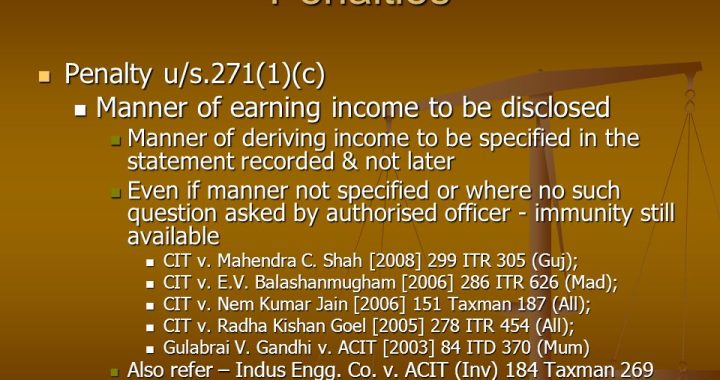

Diving Deeper: The Impact of the New Tax Bill on Dairy and Farming Income  Bombay High Court Upholds Section 271(1)(c) Penalty for Deliberate Non-Disclosure

Bombay High Court Upholds Section 271(1)(c) Penalty for Deliberate Non-Disclosure  Reporting of Foreign Assets by Indian Taxpayers under Section 139(1) of the Income Tax Act

Reporting of Foreign Assets by Indian Taxpayers under Section 139(1) of the Income Tax Act  Can an assessee pay House Rent to his parents and claim relief? Would there be any legal complications?

Can an assessee pay House Rent to his parents and claim relief? Would there be any legal complications?  Boost Your Business & Reduce Taxes: A Guide to Maximizing Benefits Under Section 80JJAA

Boost Your Business & Reduce Taxes: A Guide to Maximizing Benefits Under Section 80JJAA